Oh how an Earnings Call can ruin your day :) Cat's Earnings call left many investors wondering if the CEO was truly on their side. Other quick traders were left wondering if Bad News were in fact Bad News, now.

Let us begin to dissect.

Let us begin to dissect.

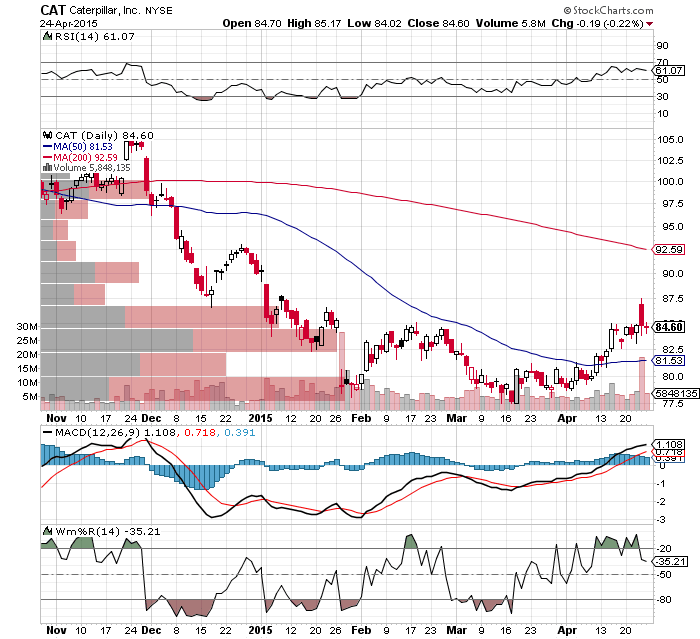

the chart

| 1. The climax and Disappointment. 2. The intact trend that is about to break. 3. The Struggle to keep or brake the long support level. 4. The Double (or even Triple) bottom. 5. The Double attempt at upper channel level. | 6. The disappointing RSI, flat. 7. The Tired MACD. 8. The Curving 50 MA. |

We are about to be locked in a multi year trade range that could be quite profitable if played correctly. Notice the up trend no.2 above. Before pounding the table on any direction here, we should wait to see how we trade against it in the coming couple days. We don't for see a reason for $CAT to climb higher up that trend but we could be surprised as positive market conditions may help this sexy kitten climb up. In anyway, if the line fails to hold, we should see a steady decline to the bottom at no.4 at the bottom of the side range.

Notice the volume per price above. We expect to have heavy selling from buyers trapped from the previous fake rally to $85. We are against smart traders here who also bought at or below $80 for a second attempt at $85. They will too sell. But also note the strong buying from investors with a hard-on every time Cat goes below $80. Those will catch you form falling.

the cheap commentary

The reason for the Earnings sell-off is simple. $CAT didn't deliver what the big investors really wanted to hear. And what was that? A pretty outlook for Machine Sales and a healthy outlook on Mining. What we received was a very unimpressive beat on low ball numbers, and a less than rosy outlook. Although Year End Revenue and EPS was guided up a little, these are still way lower than past Q2-Q4 2014 results. What will be driving this year results? Well, a super lean cost-cutting machine and those Geeks in Accounting. But Sales will remain low and suffer towards the end of the year. The bad in the good is, used and remanufactured sales are sure to pick up late 2015 and early 2016 as mining starts to buy at low borrowing costs preparing for the next awakening but those sales would hardly make the revenue needle move. On the other hand, they will definitely cannibalize new machine sales which is how Cat brings the cheese home.

For Q2-Q4 in total, Caterpillar is now guiding for $37.3 billion in revenue and $3.14 per share in profit. In Q2-Q4 of 2014, Caterpillar generated $41.9 million and $4.77 per share in net income.

" We had a solid first quarter, which led to raising the profit outlook for 2015. However, we continue to face headwinds and uncertainty in 2015, and our outlook for the year reflects that. We expect sales and profit in each of the remaining three quarters of 2015 to be lower than the first quarter. We expect sales for oil applications to decline starting in the second quarter, and from a profit perspective, the first quarter included the gain on the sale of our remaining interest in the logistics business and that won't repeat. The first quarter is usually the most seasonally favorable of the year for costs, and we don't expect the rest of the year to be as favorable. " - CAT CEO

For Q2-Q4 in total, Caterpillar is now guiding for $37.3 billion in revenue and $3.14 per share in profit. In Q2-Q4 of 2014, Caterpillar generated $41.9 million and $4.77 per share in net income.

" We had a solid first quarter, which led to raising the profit outlook for 2015. However, we continue to face headwinds and uncertainty in 2015, and our outlook for the year reflects that. We expect sales and profit in each of the remaining three quarters of 2015 to be lower than the first quarter. We expect sales for oil applications to decline starting in the second quarter, and from a profit perspective, the first quarter included the gain on the sale of our remaining interest in the logistics business and that won't repeat. The first quarter is usually the most seasonally favorable of the year for costs, and we don't expect the rest of the year to be as favorable. " - CAT CEO

The Challenges: The U.S. Dollar, Europe and Latin America, Asia competition getting stronger, and Oil and commodities prices. The challenges have already taken a hit on Cat's revenues. I will let you the reader decide on future impact. This observer's opinion? These challenges aren't going anywhere anytime soon.

So why are we Bullish about this stock? Well, we were very Bullish until we heard Cat's CEO talk. How does that change our position? Slightly, we remain Bullish on a long term plan.

Here is what we know and what Bears and Bulls can agree on: This little Kitten is experiencing another sour cycle in the industry. They do come and they do go. But, when the cycle improves, Cat will be better positioned to take the next leg up. The company is becoming a lean machine and investors should make note of that.

Will the stock go back to $100 per share? You bet it will. When? Tough one to answer. But a boring (but profitable) reason to be on the stock is the high yield they provide. And the fact that Cat is such an old-styled company that won't ever disappoint long term investors by removing or reducing the dividends. So you can be sure that, with the stock at these or even lower prices, you will be enjoying a nice 3-4% yield. We believe these, industry cycle, proactively lean efforts, and high yield, to be reasons enough to play with this sexy kitten.

So why are we Bullish about this stock? Well, we were very Bullish until we heard Cat's CEO talk. How does that change our position? Slightly, we remain Bullish on a long term plan.

Here is what we know and what Bears and Bulls can agree on: This little Kitten is experiencing another sour cycle in the industry. They do come and they do go. But, when the cycle improves, Cat will be better positioned to take the next leg up. The company is becoming a lean machine and investors should make note of that.

Will the stock go back to $100 per share? You bet it will. When? Tough one to answer. But a boring (but profitable) reason to be on the stock is the high yield they provide. And the fact that Cat is such an old-styled company that won't ever disappoint long term investors by removing or reducing the dividends. So you can be sure that, with the stock at these or even lower prices, you will be enjoying a nice 3-4% yield. We believe these, industry cycle, proactively lean efforts, and high yield, to be reasons enough to play with this sexy kitten.

our sexy bottom

Simple, if you are truly interested in a long term investment with high yield then you can start accumulating anywhere fro $75 to $82. Which is the Range we believe it will be trading for a while. No excitement, nothing to give you a hard on, I know, but a nice steady Yield nevertheless.

For those looking for a Quick and Dirty swing, look to entry at the $80 base and sell at around $85/86 prices. I wouldn't go in with less than $10k, anything less and you are wasting everybody's time.

For those looking for a Quick and Dirty swing, look to entry at the $80 base and sell at around $85/86 prices. I wouldn't go in with less than $10k, anything less and you are wasting everybody's time.

RSS Feed

RSS Feed